Is Whole Life Insurance Worth the Investment? Exploring the Pros and Cons

Whole life insurance is often touted as a solid investment option, providing not only a death benefit but also a cash value that grows over time. One of the major pros is the predictability it offers; policyholders can count on fixed premiums and guaranteed growth of the cash value. This can be particularly appealing for those seeking long-term financial stability. Additionally, whole life insurance can serve as a tool for estate planning, allowing policyholders to leave a legacy for their beneficiaries without incurring tax liabilities. However, the investment aspect comes with its drawbacks, such as comparatively high premiums and lower returns when compared to other investment vehicles.

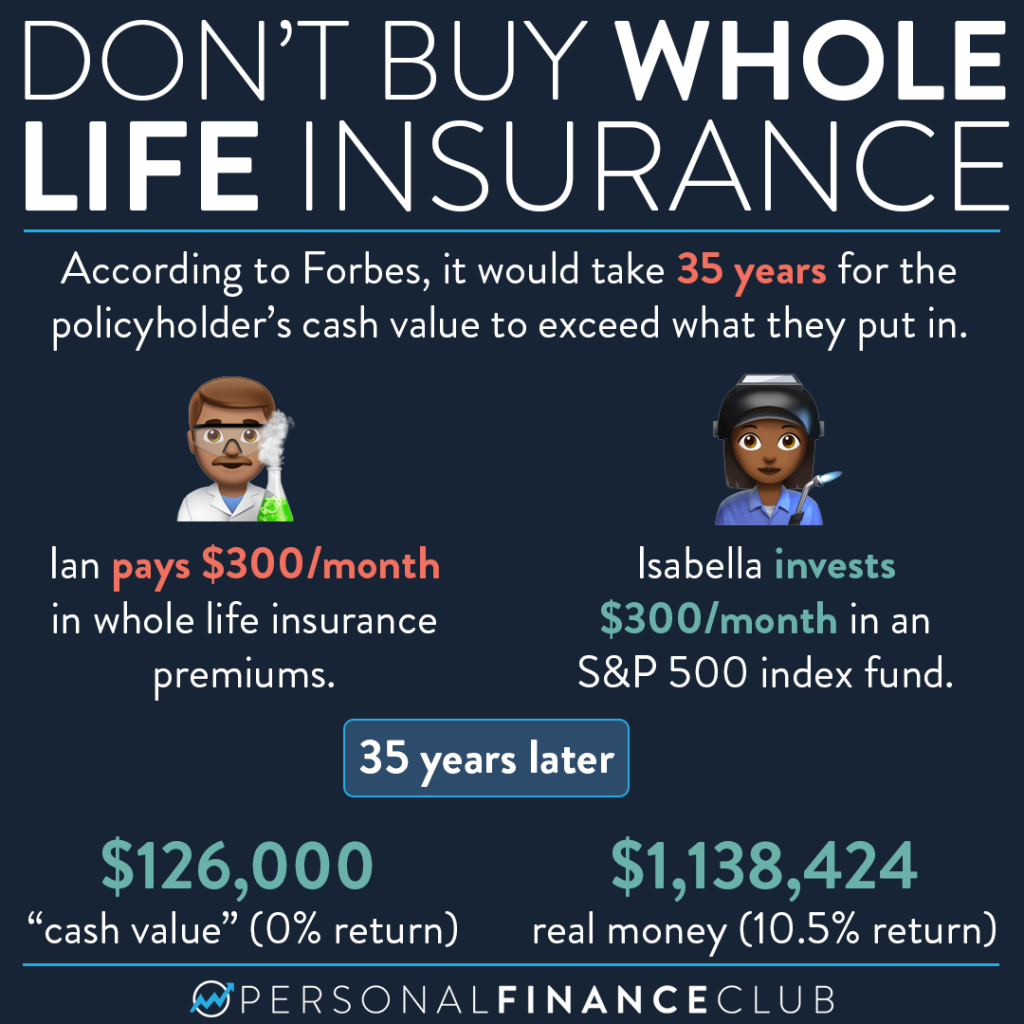

On the flip side, the cons of whole life insurance cannot be overlooked. First and foremost, the cost of premiums can be a significant financial burden over time, making it less accessible for younger individuals or those with tighter budgets. Moreover, the cash value accumulation is typically slower in the early years of the policy, which may frustrate some policyholders expecting quick returns. Lastly, critics often argue that investing in whole life insurance locks up funds that could otherwise be invested in higher-yield investments, such as stocks or mutual funds. Ultimately, balancing the pros and cons is essential in assessing whether whole life insurance is truly worth the investment.

What You Need to Know About Whole Life Insurance: Understanding Your Safety Net

Whole life insurance is a type of permanent life insurance that offers both a death benefit and a cash value component. Unlike term life insurance, which only provides coverage for a specified period, whole life insurance guarantees lifelong coverage as long as premiums are paid. This makes it a crucial safety net for individuals seeking long-term protection for their loved ones. The cash value aspect grows over time at a guaranteed rate, allowing policyholders to borrow against it if needed, thus adding another layer of financial security.

When considering whole life insurance, it's essential to evaluate how it fits into your overall financial strategy. Here are a few key points to keep in mind:

- Premiums: These are typically higher than those of term policies but remain level throughout the life of the policy.

- Cash Value Growth: This provides a forced savings mechanism, allowing you to build wealth over time.

- Dividends: Some whole life policies participate in profit-sharing, which can result in dividends that can be reinvested or withdrawn.

By understanding how whole life insurance functions, you can make informed decisions about your financial safety net and ensure you have the protection you need.

Whole Life Insurance vs. Term Life Insurance: Which is Right for You?

When choosing between whole life insurance and term life insurance, it is essential to understand the key differences between these two types of coverage. Whole life insurance provides lifelong protection and includes a cash value component that grows over time, which can be borrowed against or withdrawn. In contrast, term life insurance offers coverage for a specified period, typically 10, 20, or 30 years, and pays a death benefit only if the insured passes away during the term. Many individuals opt for term life insurance due to its lower initial premiums, making it an attractive option for those seeking affordable coverage during critical life stages, such as raising children or paying off a mortgage.

Determining which type of policy is right for you depends on several factors, including your financial goals and current circumstances. If you require a policy that builds cash value over time and provides lifelong coverage, whole life insurance may be the better choice. Alternatively, if your primary goal is to ensure financial protection for your loved ones during a certain period without the high premiums associated with permanent policies, term life insurance might be more suitable. Ultimately, assessing your long-term needs and consulting with a financial advisor can help you make an informed decision that aligns with your personal and financial objectives.