Understanding the Hidden Benefits of Term Life Insurance

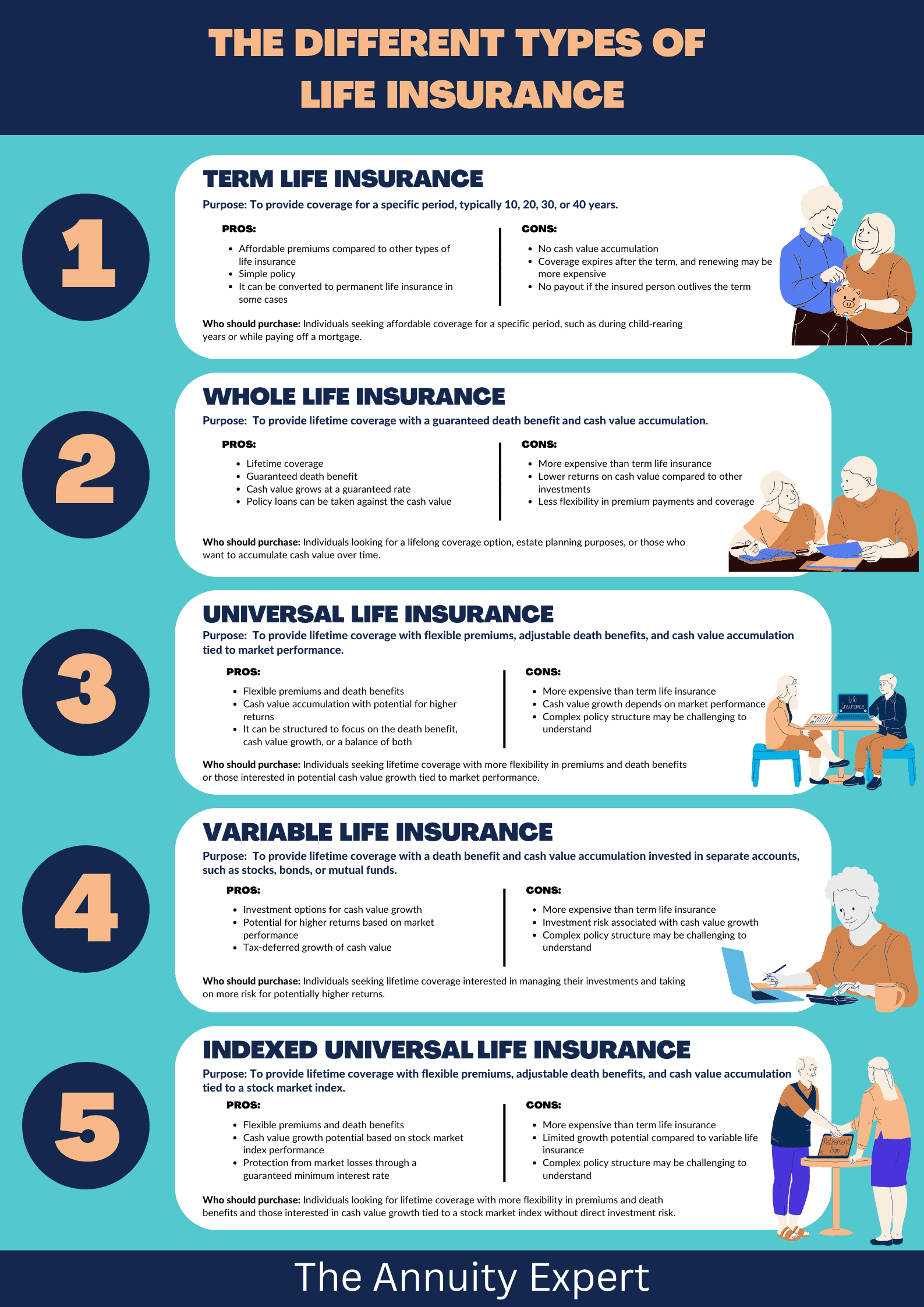

Term life insurance is often viewed primarily as a safety net for families in the event of unexpected loss. However, there are various hidden benefits that can significantly enhance its value. One of the primary advantages is its affordability; compared to whole life insurance, term life policies typically offer lower premiums, allowing policyholders to allocate their finances more efficiently. This affordability means that individuals can secure substantial coverage without straining their budget, potentially freeing up funds for other important investments or savings goals.

Additionally, many term life insurance policies come with conversion options, enabling policyholders to convert their term coverage to a permanent policy without undergoing further medical underwriting. This feature can be invaluable for those who may develop health issues later in life, ensuring continued coverage when it is needed most. Furthermore, some term policies offer added benefits like living benefits or accelerated death benefits, allowing terminally ill policyholders to access a portion of their death benefits while still alive, providing financial support during difficult times.

Is Term Life Insurance the Best Choice for Your Family's Financial Security?

When considering your family's financial security, it is crucial to evaluate the benefits of term life insurance. This type of insurance offers coverage for a specific period, typically ranging from 10 to 30 years, and is designed to provide financial support to your beneficiaries in the event of your untimely passing. Unlike whole life insurance, which builds cash value over time, term life insurance tends to have lower premiums, making it an appealing option for families on a budget. This affordability allows policyholders to maximize their coverage, ensuring that their loved ones have the financial resources needed for expenses such as mortgage payments, education, and daily living costs.

However, it’s important to consider your long-term goals when choosing term life insurance. While the lower costs are attractive, many families may find themselves without coverage once the term expires, particularly if their financial situations change or if they develop health issues. To determine if term life insurance is the best choice for your family, ask yourself the following questions:

- What are your family's financial needs in the event of your passing?

- How long will these needs last?

- Can you afford to convert to a permanent policy later if necessary?

Top Reasons Why Term Life Insurance is Essential for Financial Peace of Mind

When considering your family's financial future, term life insurance stands out as a crucial component. It provides a safety net that can replace lost income, cover debts, and ensure that dependents maintain their standard of living in the event of an untimely death. Here are the top reasons why term life insurance is essential for achieving financial peace of mind:

- Affordability: Compared to whole life policies, term life insurance is generally more affordable, allowing individuals to secure substantial coverage at a lower cost.

- Clear Coverage Period: Since term life insurance is designed to provide coverage for a specific period, it aligns well with major financial responsibilities, such as raising children or paying off a mortgage.

Moreover, another significant factor contributing to the importance of term life insurance is its simplicity. Policies can be straightforward, making it easier for individuals to understand their coverage and benefits. Furthermore, having a term policy can lead to peace of mind, knowing that your loved ones will not face financial hardships in case of your absence. In conclusion, securing term life insurance is a proactive step toward ensuring that your family remains financially stable, allowing you to focus on what truly matters.